“It’s a collateralized debt obligation [CDOs] made up out of, like, C-rated mortgages,” said Wesley Yang in a conversation with John Sailer in 2022. “These people, their job is—as the rating agency—to say that it’s all A plus.”

Yang and Sailer were not talking about the CDOs stuffed with subprime mortgages and fraudulently passed off as safe, which eventually led to the collapse of the housing market in 2008. Rather, they were talking about the medical literature on gender, how clearly fraudulent it is, and more broadly about what our universities have become. For many working outside of finance “collateralized debt obligation” might as well be synonymous with “college degree,” the collateral in this case being one’s financial future and freedom. And like the housing market bubble before it, the higher education bubble is ready to burst.

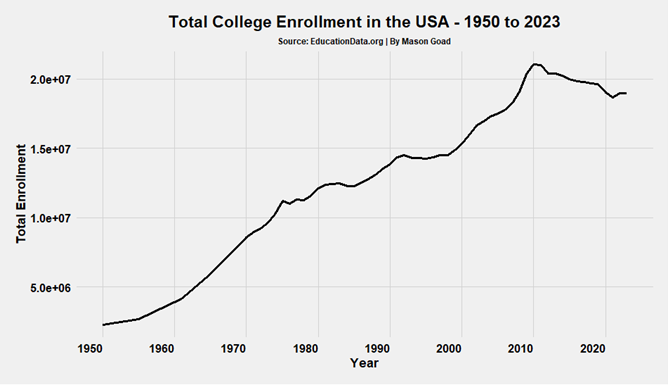

Beginning in the 1960s, American colleges and universities began accepting more students, and between 1965 and 1975, the number of students and professors hired to teach them doubled. “It was as if the United States took a century to build one system of higher education, and then, in a single decade, built a second one of the same size,” said Dr. Lyell Asher in the 2022 micro-documentary Why Colleges are Becoming Cults. The fact that many of these new students and professors viewed the academy as a base for activism rather than for education also hurt the preservation of the university’s true mission and societal function.

Worse, the doubling of the American higher education system brought in students who should never have been enrolled, much less graduated.

Recently, a meta-analysis of undergraduate students found that the average IQ of undergrads has declined precipitously over the years, and recent data indicate that the average undergrad now has an IQ equivalent to the average IQ of the general population. As the authors of the study explained: “[t]he decline in students’ IQ is a necessary consequence of increasing educational attainment over the last 80 years. Today, graduating from university is more common than completing high school in the 1940s.”

Many of these incapable but credentialed students end up as university administrators with nowhere else to go in the private sector. A 2021 study found that between 1976 and 2018, full-time faculty increased by 92 percent and students by 78 percent, while “full-time administrators and other professionals employed by those institutions increased by 164% and 452%, respectively.” Today, many of these administrators, with hollow and/or fraudulent academic credentials, lead our universities. The most notable example is Claudine Gay, Harvard’s former president, who was appointed with only 12 publications and who resigned after she was revealed to have plagiarized several times.

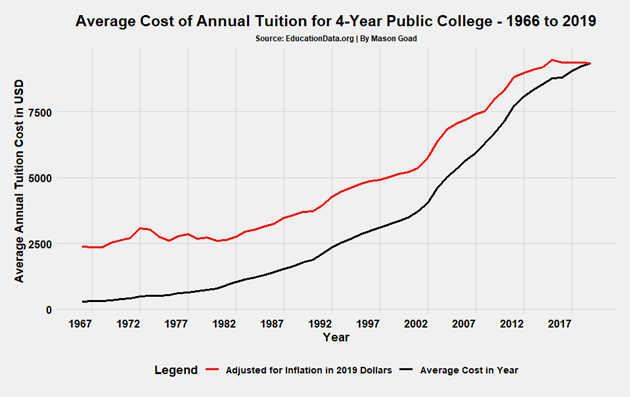

The decline of college students’ cognitive abilities has significantly diminished the signaling power of a college degree, but thanks to the rise in unnecessary administrators, the cost of obtaining a degree has increased dramatically. In fact, looking at historical data, the cost of attending college has far surpassed the rate of inflation. The average annual cost of tuition for a four-year public institution was $302 in 1966, which is $2,386 in 2019 dollars. But by 2019, the average cost of tuition was $9,349, about four times greater even when all data points are adjusted for inflation.

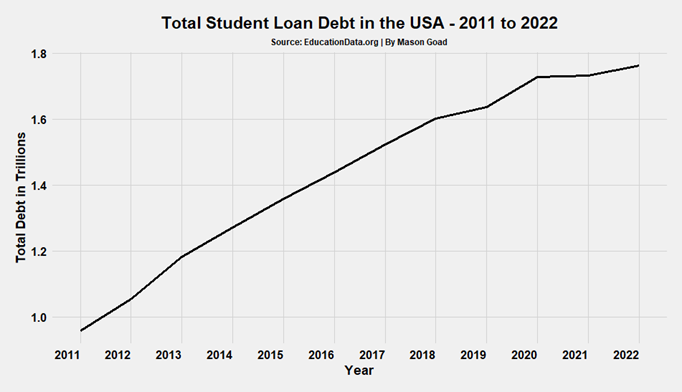

These increased costs have consequences for the many students who see college as a necessary convention for their careers. As Neetu Arnold explained in her 2021 NAS report, Priced Out: “Young Americans paying off student loans delay personal milestones such as buying a house, getting married, or having children… Young Americans devote their talents to paying off debt rather than to creating a future for themselves and for their country.” And young Americans have continued to accumulate that debt. As of 2023, Americans now owe 1.73 trillion dollars in student loan debt. The total amount of student loan debt nearly doubled between 2011 and 2022.

The government has not addressed the devaluation of a college degree, nor the administrative bloat, nor the rising costs and rampant borrowing that has led to the student debt crisis. Instead, the government has, in effect, sought to bail out the universities—just as it bailed out the banks. The Biden administration began 2024 with the announcement of 4.9 billion dollars in student debt relief, but that would barely put a dent in the 1.73 trillion dollar total. Cancelation of student debt will not resolve the underlying issues that caused the debt crisis, nor is it intended to. The intent is to pander to voters and deflect attention away from the universities that scammed them.

Serious reforms are needed, too few are being implemented, and so, just like the housing bubble, the higher education bubble will eventually burst. The question is not if but when and how suddenly it will occur. If it happens suddenly enough, those guilty of fraud will plead innocence, the authorities who should have known better will plead ignorance, and millions of indebted Americans will be left with unrealized dreams of jobs, future homes, and happy families—just like last the last time.

Photo by Jared Gould — Adobe — Text to Image

Most of the brightest young minds these days are actively avoiding the University system due to the implied liability of going into debt acquiring a nearly worthless degree. With next to no social safety net in place; this is, in fact, a very rational and wise decision. If we are not already in this state we will soon be in the state where a University degree merely signals that you came from a rich family; not unlike the titles of nobility in ages past. An uneducated population is an unproductive population.

One other thing: “It’s a collateralized debt obligation [CDOs] made up out of, like, C-rated mortgages,” said Wesley Yang in a conversation with John Sailer in 2022. “These people, their job is—as the rating agency—to say that it’s all A plus.”

There is a big difference here — a mortgage, regardless of how deeply “underwater” or how shaky the debtor, is still guaranteed by a piece of real estate which can be foreclosed upon and sold for some value.

The 13th Amendment frowns on slave auctions — there is no way to foreclose upon the student to secure the student loan. Within limits, you can take whatever liquid assets the student has, but these limits (intended to ensure basic sustenance) are usually more than the person has. You can’t foreclose on the person’s soul.

In a more realistic light, while you can withhold transcripts and destroy the person’s credit rating, all you really are doing is destroying the person’s ability to make a living. And while one may feel good about this on a micro level, what is the cumulative effect of this? These are people who were ambitious to go to college — whatever college may be — and what are the implications of them either not able to earn a living and/or having whatever they earn garnished away from them?

If they are female, a lot of them will quickly get pregnant. It’s easy enough to do and while the ideal is to have a rich man father your child — a mistake that many young ladies made when the lobster industry imploded a while back — but even if you tell the state that you don’t know who the father is, you’ll still get a benefits package that (with taxes) you’d have to be earning $55K-$60K to have. You have a car, you have a modest apartment or house, you’re eating fairly well, and you have free medical care.

And if they are male, they go into any variety of sketchy things, ranging from the outright illegal (dealing drugs) to some of the really sketchy construction companies and the rest.

Or they instead work at Starbucks, knowing that they aren’t making enough to be garnished.

And while a bank may have to hire someone to go mow lawns every few weeks if the municipality plays hardball, foreclosed homes are allowed to sit to decompose.

By contrast, foreclosed persons still have to be fed, housed, and provided medical care.

And there is NO guarantee that they will EVER be worth anything.

My point is that a foreclosed property is still an asset that may eventually have value. (I know of a major Massachusetts landowner who bought up the deeds to farms in the Depression and became a forestry magnate.)

But a foreclosed person is a liability — TO SOCIETY — and while that may not show up on the balance sheet, it is still going to be an issue that society has to deal with.

Lots of people are upside/down on student loans — they owe more than the education is worth. That’s not going to end well…. We’re going to have to feed & house them…

“Beginning in the 1960s, American colleges and universities began accepting more students, and between 1965 and 1975, the number of students and professors hired to teach them doubled.”

We need to be accurate — take a look at the changing US Birth Rate for the 20th Century:

https://upload.wikimedia.org/wikipedia/commons/thumb/6/66/US_Birth_Rates.svg/800px-US_Birth_Rates.svg.png

The stock market crash of 1929 didn’t hurt Middle America as much as the subsequent bank failures and you can see birth rates plummet in the early 1930s. The same thing happened to college enrollment — the Amherst College Yearbooks of that era list the names and addresses of class members forced to withdraw “due to the economic situation.”

The war ended in 1945, the peak of the “Baby Boom” was in 1948 and 18 years later — in 1966 — the Baby Boomers were ready to go to college. Now this is births per thousand adults, a more difficult figure to work with, but you can see it going from 18.5 in 1935 to 26.5 in 1948. Hence absent any Higher Ed Act, there would be a lot more 18-year-olds in 1966 than there had been in 1935.

Even if the cohort percentage enrolled in higher education remained constant, enrollment would have increased, I don’t have a problem with the number of students and professors doubling between 1965 and 1975 — nor with it remaining constant into the early ’80s because that’s when a lot of women went to college.

You will notice that your debt really doesn’t start spiking upward until the mid ’80s and I think this is the point you should have made. Not that colleges expanded to meet demand, but that they didn’t downsize when the demand disappeared

I look at college costs a little differently — the minimum wage in 1966 was $1.25 and ignoring deductions, $302 could be earned in 241.6 hours or six 40-hour weeks.

The Federal Minimum Wage in 2019 was $7.25 which means that $9,349 can be earned in 1290 hours, or thirty-two and a quarter 40 hour weeks. This is why students have 2 or 3 jobs during the school year as well.

The real problem is that almost all the Baby Boomers had their babies in the late ’80s & early ’90s and that “boomlet” became “The Millenials” that colleges expanded for and that was the real fatal mistake because they did a lot of building with borrowed money, and hired a lot of people they politically can’t fire.

Forget academic standards, there aren’t enough warm bodies to fill the seats — and this will get very interesting in the fall of 2026…

It’s going to implode — of that I have no doubt — I just don’t want to leave them any excuses and hence my mention of the Baby Boom demographics.