The notion that states have been cutting funding for higher education, commonly referred to as state disinvestment, is widespread within academia and the media. These cuts are alleged to be responsible for much of what ails higher education, especially the rise in tuition. Consider, for example, some recent statements from education leaders:

• James Kvaal, President Biden’s undersecretary of education, stated that “we’ve had states disinvesting for decades now.”

• Ted Mitchell, president of the American Council on Education, wrote that “over the past several decades, many state legislatures have largely walked away from their responsibility to provide adequate funding for their states’ public universities. State disinvestment is a major driver of rising tuition prices at public colleges and universities—and a big reason why many students have been forced to borrow more to pay for college.”

• Kevin Miller, associate director of higher education at the Bipartisan Policy Center, wrote that “college costs and student debt continue to rise, and cuts in state funding for higher education have been a major reason why.”

These are not one-off tweets by random strangers, but authoritative statements from people who’ve been in the industry for years and who should have an accurate view of long-term trends. Moreover, they are repeating what’s been the conventional wisdom for years, namely, that states have been disinvesting in higher education for decades.

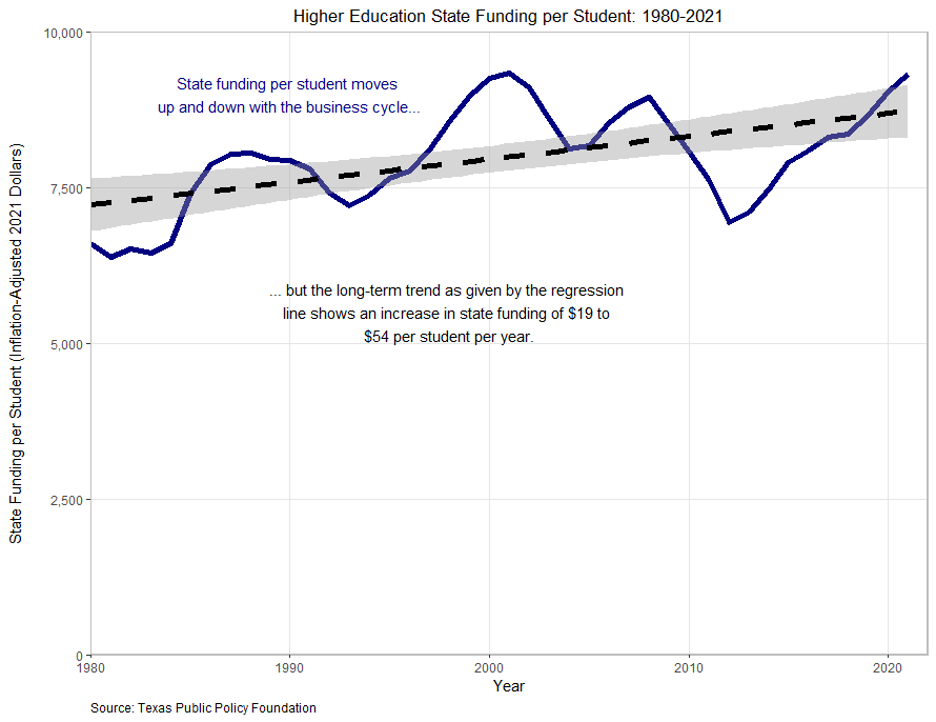

There’s just one problem—state disinvestment is a myth. In this case, a picture really is worth a thousand words, so just look at the graph below, reproduced from my new report that shows inflation-adjusted state funding per student from 1980 to 2021.

If state disinvestment were real, then there should be a clear downward trend. Not only is there no downward trend, but the statistical evidence points 180 degrees in the opposite direction—there is, in fact, an upward trend. In other words, far from disinvesting, states have been increasing their investments in higher education over the last four decades.

The conventional wisdom is wrong. State disinvestment is a myth.

[Related: “GI Bill Benefits are Compensation, Not a Loophole”]

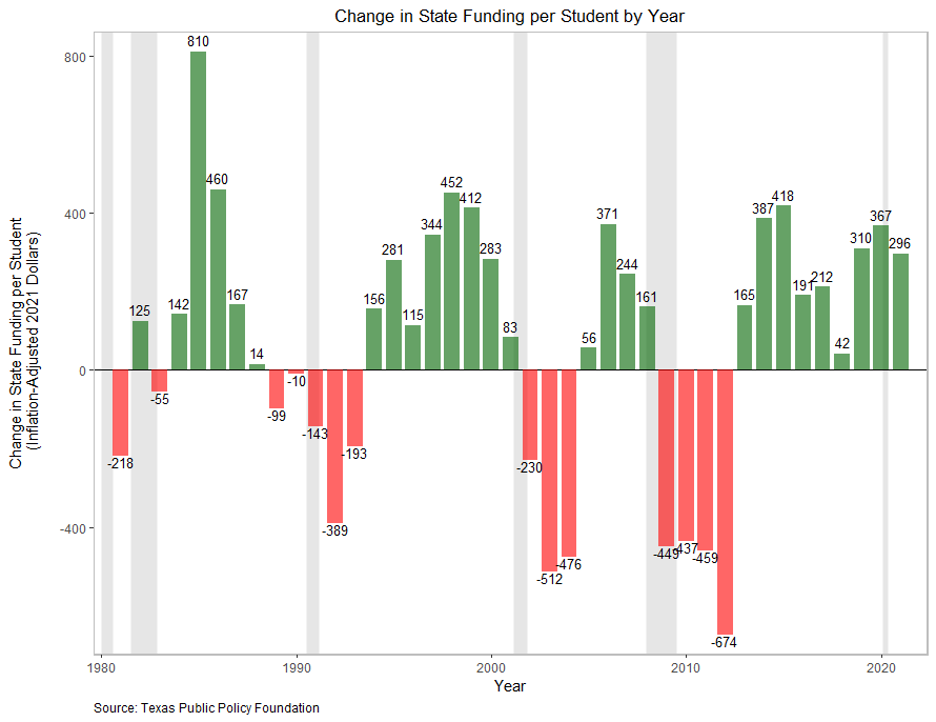

There are two main reasons why the belief in state disinvestment is so widespread. First, as the second graph (also reproduced from the new report) shows, there are times when states do cut funding, typically during and after recessions (indicated by the grey vertical lines). If you asked a college administrator about state funding in 2012, he would have just experienced some of the largest cuts in history for four straight years. These cuts get a lot more attention than the slow and steady increases in normal years, leaving the impression that funding declines are typical—even though they aren’t.

The second reason many people believe in state disinvestment is a failure to adjust for inflation. Most claims of disinvestment cite the annual State Higher Education Finance (SHEF) report published by the State Higher Education Executive Officers Association (SHEEO). The SHEF report does not adjust for inflation using a standard price index like the Personal Consumption Expenditures Price Index (PCE). Instead, it uses a homemade price index, the Higher Education Cost Adjustment (HECA), to adjust for costs. Needless to say, this is not standard operating procedure, and it leads to completely unreliable estimates. As I wrote in the new report,

the HECA adjustment thus overestimates state funding in 1980 by almost $2,500. By overstating past funding, HECA is heavily biased toward finding state disinvestment. This bias is so strong that even if state funding increased by $2,000 per student, the HECA adjustment would record that as a decline.

As an aside, what is SHEEO’s response to my legitimate criticisms? SHEEO’s Sophia Laderman claims that my “paper is really trying to cherry pick and push a narrative.” The charge of cherry-picking is either remarkably uninformed or a lie. Cherry-pickers love to choose beginning and ending dates that conform to their story. Yet my paper uses two methods that make cherry-picking impossible. First, I used all available data, spanning four decades. If you cut down the whole orchard, you aren’t cherry-picking. Second, I use a regression to determine the long-run trend. Regressions are not unduly swayed by beginning and ending values. Either of these would render the charge of cherry-picking false. Using both, as I did, renders the charge laughably dishonest. Either Laderman doesn’t know this, which is concerning, or she does know it and chooses to make false accusations anyway, which is even more concerning. As for the narrative I’m pushing, I’m searching for the truth by following the data, something I would hope SHEEO tries to do as well.

It is alarming that the consensus view on state funding—that it has been decreasing for decades—is so out of touch with reality. Most people probably cite the SHEF report without realizing that it doesn’t adjust for inflation. Others suffer from confirmation bias, uncritically accepting any information like the SHEF report that is consistent with their preconceived notion that states have cut funding. And a few may know better but choose to spread disinformation because it advances their ideological or political cause.

[Related: “Student Loans Cost Taxpayers $645 Billion More Than We Were Told”]

Misjudging the direction of historical state funding will obviously affect policy decisions regarding future funding, but the flawed conventional wisdom distorts other policy conversations as well.

Improving college affordability should be a high public policy priority, so the question of why tuition has increased so much is of crucial importance. According to state disinvestment proponents, the answer is simple. Tuition increases to make up for state funding cuts (see the Mitchell and Miller quotes above). But this couldn’t be further from the truth. Tuition has been increasing, but so has state funding. If tuition changes to offset changes in state funding, then tuition should be falling, not rising. For example, in 1980, state funding per student was $6,605. In 2021, it was $9,327. If tuition merely offsets changes in state funding, then tuition should have fallen by $2,722. Instead, tuition rose by almost $5,000 (from $1,745 to $6,723). Clearly, increases in tuition cannot be explained by nonexistent cuts to state funding.

By garnering most of the attention, though, the flawed state disinvestment explanation suffocates other more plausible explanations for the rise in tuition. Until the conventional wisdom on state disinvestment changes to reflect the truth—that state disinvestment is a myth—we will continue to misdiagnose the causes of declining college affordability.

Image: acarapi, Adobe Stock

What UMass did was increase student fees in the years when the state cut the budget and then maintained the increases in years when the state increased the budget.

Another trick was to spend already-allocated money for something else, eg new buildings, and then threatening

mid-year tuition increases if the state give them a supplemental allocation to fund what the legisature HAD ALREADY FUNDED ONCE.

And then they adopted the logical fallacy of claiming that a decreased percentage of a much larger total constituted a cut when state funding actually increased — adjusted for inflation.

UMass was unique in that it had done very well during the 1980’s when Reagan’s defense buildup funded lots of high-tech along Route 128. But when the Cold War ended, the money all dried up and unlike other state agencies, UMass essentially tripled student costs via a mosiac of new fees that only have been increased 30+ years later.

Andrew Gillen makes a pretty silly argument here. Of course, a personnel-heavy service function like higher education is probably going to rise in cost faster than the CPI rate of inflation. Read up on Baumol’s law. It doesn’t just apply to higher education. Take a look at medicine! The actual cost of higher education has risen a bit faster than the rate of inflation for decades. Why is this? Well, costs for professional salaries have risen for decades. That applies to professors as well as other professionals. Then there’s the rising cost of medical care. Yes, professors expect good medical insurance. And guess what, the janitors demand the same. (I guess they could all be put on Medicaid like fast food workers who get sick.) And then, people want better amenities. Students would blanch at the slop that we used to get in the dorms. Ditto the primitive dorm rooms of old, the ancient classrooms.

The thing to really look at is state budgets, the share of GDP going to higher education, etc. I think you’ll find that state budgets have been shifted to other things like medicaid. The share of GDP probably about constant.

Sure, you can fantasize about running colleges with 1950’s budgets. Ditto with K-12 schools. You’ll do a double take at how absurd that would be if you look at the numbers.

In the1950’s, professors taught 8 classes a year. Today they teach far fewer….

Probably some truth to that. Eight classes (4 per semester?) sounds like a lot, but some people do get stuck doing that even today, even some tenure-track people at small struggling schools.

The classes take much more time now than they used to, and are much harder to teach, for a variety of reasons. Even compared to the 80’s and 90’s. And then of course covid made everything much harder.

Somehow in all this I missed what you find so silly in his argument. His argument is that “state funding has decreased so tuition has had to increase” is untrue. He makes the case well. Looking at the fraction of a state’s GDP going to IHEs is irrelevant to what he is arguing. However, I think you may be suggesting a reason for at least part of the increase in tuition: competition for a diminishing pool of students. Add to that the near-explosion in the number of administrators at the bigger IHEs and I think you’ve got the cause of cost increases nailed!

What is silly about his argument, which you don’t seem to get, is tying increases in higher education costs to the consumer price index. The costs are just going to go up faster than the CPI. Education is not something that can just be automated like a factory. A lot of people — other silly people — have tried, but it doesn’t work.

You would understand all this if you were running a university that had to pay competitive salaries, rapidly increasing medical costs, modernized facilities.

Same thing applies, actually, to your local K-12 school. Try running it at about 1/4 of its present budget. You will not succeed. But 4x is about how much it has increased (in inflation-adjusted dollars) over the past 50 or so years.

Detroit circa 1969 — both labor & management doing well and neither caring about the inferior & overpriced product consumers had to purchase.

Then the Japanese cars arrived…,