Andrew Gillen is a Research Fellow at the Cato Institute.

As artificial intelligence (AI) models continue to expand their capabilities and their usage spreads, more cases of bias are emerging. It is essential to determine whether its biases are valid or have been introduced by human interference, whether deliberate or accidental. Once we know the source of the bias, we can hopefully find remedies. AI […]

Read More

The reconciliation bill is shaping up to be the boldest legislative change in higher education in decades. But it is still in an early stage, with the House having passed its version, and the Senate hoping to do so soon. Next will come negotiation to work out any differences between the House and Senate versions, […]

Read More

The House of Representatives has passed its version of the reconciliation bill, which includes a new accountability system for higher education. Under this system, colleges would be responsible for reimbursing the government for a share of the government losses on loans to their students, with the share being determined by the college’s cost relative to […]

Read More

One of the best parts of the higher ed portion of the reconciliation bill being pushed in the House of Representatives is a shift from cost of attendance (COA) to median cost of attendance (MCOA). What is the Cost of Attendance and Why Does It Matter? COA is the total cost of attending college, including […]

Read More

The American Enterprise Institute and the Heritage Foundation have released a new booklet of advice for university trustees. My short contribution focuses on how trustees can reduce university spending and personnel and offers nine recommendations which I summarize below. Recommendation #1: Have a Specific and Measurable Goal A clear, specific, and measurable goal is […]

Read More

Scarcely a week goes by lately without news that another university has had federal funding restricted by the Trump administration. The Wall Street Journal recounts that latest restrictions: “Harvard ($2.26 billion), Cornell ($1 billion), Northwestern ($790 million), Brown ($510 million), Columbia ($400 million), Princeton ($210 million) and the University of Pennsylvania ($175 million).” These actions […]

Read More

Shifting student loans from the current government-as-lender model to the private market would be beneficial. As I recently reported, this shift would reduce malinvestment—educational spending that doesn’t justify its costs—while increasing accountability for colleges, improving incentives for both students and institutions, and fostering more informed decision-making through price differences. But privatization is a broad bucket. […]

Read More

Higher education accreditation is an arcane but vitally important target for reform in the new administration. Accreditation is used to ensure colleges meet a minimal level of quality—colleges without an accreditor approval do not have access to federal financial aid programs like Pell Grants and student loans. But accreditation is broken. As I lay out […]

Read More

The National Institutes of Health (NIH) announced that it is cutting indirect costs to a maximum of 15 percent. What should we make of this effort? Let’s begin by asking a simple question: what are indirect costs? For a research project, there are some costs that are directly attributable to that project such as the […]

Read More

Usage of artificial intelligence (AI) models is rapidly spreading in education. Students use them to help with their coursework, and teachers and faculty use them to help with lesson plans and research. To the extent that these models can act as a tutor for students or an assistant for teachers and faculty, they can be […]

Read More

Republicans have their best opportunity in decades to significantly reform or even eliminate government involvement in student loans. As I explain in a new Cato Institute paper, doing so could generate up to $212 billion in savings over the next ten years. But Congress needs to act quickly as the window of opportunity will close […]

Read More

With the elections in November giving Republicans small majorities in the House and Senate, there is considerable attention on potential reconciliation bills with pros and cons relative to regular legislation for the new Republican majorities. On the bright side, reconciliation bills cannot be filibustered, which means that they only need 51 votes rather than the […]

Read More

Most of the problems with student loans are due to a misalignment of incentives. There are three parties to a student loan: the student, the lender—meaning the federal government because we use a government-as-lender system—and the college. A good student loan system would align the incentives so that no party can benefit by making the […]

Read More

The College Board’s annual release of the Trends in College Pricing and Student Aid always contains a wealth of information on the latest enrollment and financial data for higher education. It is also notable that this report is much more informative, useful, and usable than anything put out by the Department of Education. If you […]

Read More

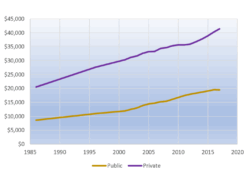

For decades, there have been complaints that states have been cutting funding for colleges, often referred to as state disinvestment. But in my annual report tracking trends in state funding, I show that state disinvestment is a myth. The figure below shows state funding per student over the past 43 years. The dashed blue regression […]

Read More

The fight over student loan forgiveness has consumed most of the attention of the higher education policy world, and as a result, other policies are receiving much less attention than they should. One such neglected topic is borrower defense to repayment, which is a method of waiving repayment requirements for student loan borrowers who were […]

Read More

Amy Wax has provided a perfect test case for accessing the state of academic freedom. On paper, just about any college would be lucky to have her. She earned both an MD and a JD, argued 15 cases before the Supreme Court, and then became a law professor at a top college for three decades. […]

Read More

Many students who planned on using federal student aid like Pell Grants and student loans to attend college this year faced an unexpected obstacle: the Free Application for Federal Student Aid (FAFSA). The FAFSA had long been criticized for being too long and complicated, so in December 2020, Congress passed the FAFSA Simplification Act. The […]

Read More

The Biden-Harris administration’s pursuit of student loan forgiveness has moved from persistent to relentless and can now only be described as reckless. To briefly recap, the administration announced its first plan back in 2022, which the Supreme Court ruled was illegal in 2023. Their second plan, a loan forgiveness scheme disguised as a loan repayment […]

Read More

Editor’s Note: The following article was originally published by Cato Institute on September 3, 2024. With edits to match MTC’s style, it is crossposted here with permission. Note, this post updates last month’s post. The biggest changes from last month include: The Supreme Court has let the Eighth Circuit’s pause on the SAVE plan remain in place. Reworked the student […]

Read More

While the Biden administration has at least nine plans to forgive student loans, some are much bigger than others. And the two biggest have now run into legal buzzsaws. The Supreme Court (SCOTUS) eventually threw out its first plan in 2022. The second plan introduced a new income-driven repayment plan called SAVE, which, in practice, […]

Read More

Editor’s Note: The following article was originally published by Cato Institute on August 1, 2024. With edits to match MTC’s style, it is crossposted here with permission. Note, this post updates last month’s post. The biggest changes from last month include: the 8th Circuit Court of Appeals halting the Saving on a Valuable Education (SAVE) plan; added insights from Jason […]

Read More

Editor’s Note: This article was originally published by Cato Institute on July 1, 2024 and is crossposted here with permission. Note, this post updates last month’s post. The biggest changes from last month include: Update on the lawsuits regarding the SAVE plan to reflect the court injunctions. Update on the prospects of the SAVE and HEA plan in light of […]

Read More

Editor’s Note: This series is adapted from the new paper Higher Education Subsidization: Why and How Should We Subsidize Higher Education? Part 1 explored the justifications and rationales that have been used to subsidize higher education. Part 2 explored subsidy design considerations. Part 3 explored federal subsidies. This fourth and final part explores state subsidies. […]

Read More

Editor’s Note: This series is adapted from the new paper Higher Education Subsidization: Why and How Should We Subsidize Higher Education? Part 1 explored the justifications and rationales that have been used to subsidize higher education. Part 2 explored subsidy design considerations. This part explores federal subsidies. The federal government provides five main types of […]

Read More

Editor’s Note: This article was originally published by Cato Institute on June 3, 2024 and is crossposted here with permission. Note, this post updates last month’s post. The biggest changes from last month include: Updated total loan forgiveness figures ($167 billion for 4.75 million borrowers) to account for the latest developments. Update on the Mackinac and Cato lawsuit, and the […]

Read More

Editor’s Note: This series is adapted from the new paper, Higher Education Subsidization: Why and How Should We Subsidize Higher Education? Part 1 explored the justifications and rationales that have been used to subsidize higher education. This part explores subsidy design considerations. There have been seven main justifications for subsidizing higher education: Promoting favored religions, […]

Read More

Editor’s Note: This series is adapted from the new paper Higher Education Subsidization: Why and How Should We Subsidize Higher Education? Part 1 explores the justifications and rationales that have been used to subsidize higher education. Higher education has long been subsidized by the government in America, but the reasons used to justify subsidization have […]

Read More

Editor’s Note: This article was originally published by Cato Institute on May 1, 2024 and is crossposted here with permission. Note: This post updates last month’s post. The biggest changes from last month include: The newest plan relying on regulatory changes under the Higher Education Act has been released and is summarized. A new court case against the SAVE plan […]

Read More

Editor’s Note: This article was originally published by Cato Institute on April 24, 2024 and is crossposted here with permission. Immediately after the Supreme Court overturned his last big student loan forgiveness plan, President Biden announced a new effort that would rely on a different law, an effort that is now nearing completion. The administration has released the draft regulations that would […]

Read More